Securing health insurance in Lebanon has become more critical than ever. With the economy fully dollarized and medical inflation rising by over 23% in the last year alone, depending only on public funds or out-of-pocket payments is a major financial risk.

For this reason, private health insurance is not just a luxury; it’s a vital investment in your health and financial security. At The Guardian, we fully understand the challenges faced by individuals and families seeking reliable healthcare coverage in Lebanon.

Therefore, this guide will help you understand health insurance in Lebanon and make wise choices, so that you and your loved ones can get the care you need without financial ruin.

For more information, you can contact our team of experts.

Why Private Health Insurance is Essential in Lebanon

The current healthcare landscape in Lebanon presents significant challenges.

For example, public health funds (like the NSSF) have seen their purchasing power collapse, often covering only a small percentage of actual hospital bills. Private hospitals now require payments in Fresh USD.

As a result, patients without private insurance often have to pay huge cash deposits before admission, which can be a heavy financial burden during an illness or accident. For a deeper look at the public healthcare system in Lebanon, you can refer to reports from the Ministry of Public Health.

Key Reasons to Invest in a Private Health Insurance Plan

1. Access to Quality Care: Private plans offer access to trusted hospitals, clinics, and specialists in Lebanon. This ensures you get quick access to high-quality medical services without long waiting lists.

2. Financial Protection: A quality health insurance plan in Lebanon shields you from unexpected and potentially enormous medical bills for hospitalizations, surgeries, diagnostic tests, and expensive medications.

3. Peace of Mind: Knowing you have coverage reduces the stress of medical emergencies, allowing you to focus on getting better rather than worrying about the bill.

4. Tailored Solutions: Private insurers provide flexible plans that can be customized to fit your needs, family size, and budget—ranging from “In-Patient Only” policies to comprehensive “Class A” coverage.

Understanding Your Health Insurance Plan Options

- In-Patient Coverage: This is the core of most plans, covering medical expenses that happen during a hospital stay. Specifically, this includes hospital room and board, surgical fees, anesthesia, and doctor’s fees.

- Out-Patient Coverage (Optional Add-on): This covers medical services that don’t require an overnight hospital stay. It usually includes doctor’s consultations, lab tests, radiology, and prescribed medications. Note: This significantly increases the premium.

- Maternity Coverage: Typically an optional add-on that covers expenses related to pregnancy, childbirth, and newborn care. Important: This almost always comes with a 10-12 month waiting period, meaning you must be insured before getting pregnant.

- Chronic Disease Coverage: This is for pre-existing or long-term conditions like diabetes or heart disease. Sometimes it’s included in comprehensive plans or as an add-on, but it often has a waiting period of 6 months to 3 years depending on the insurer.

- International Coverage: Some premium plans provide coverage for medical treatment outside of Lebanon. This is especially helpful for frequent travelers or those looking for specialized care abroad.

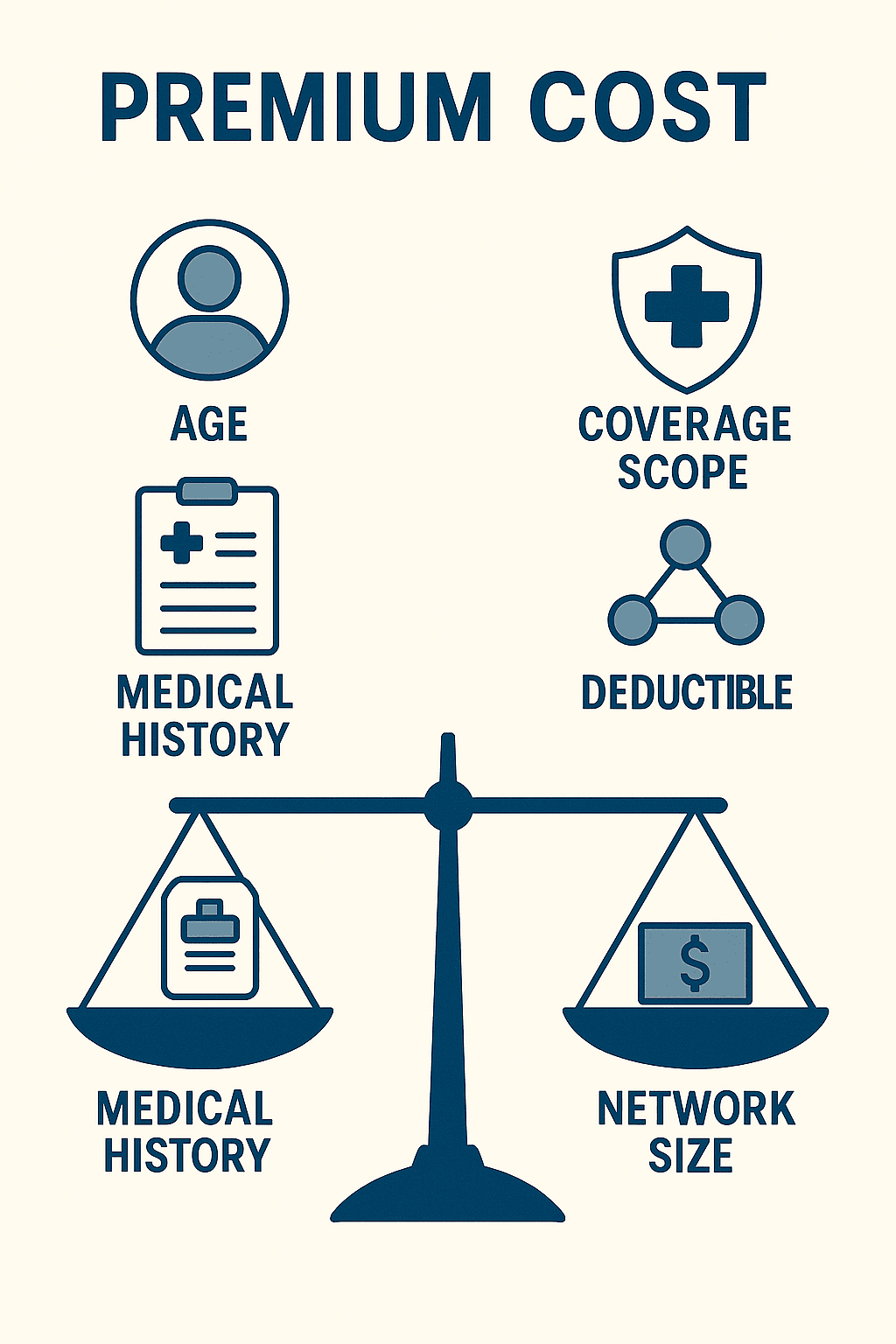

Factors Affecting Your Health Insurance Premium

- Age: Premiums generally increase with age, because the likelihood of needing medical care rises.

- Medical History: If you have pre-existing health issues, your premium may be higher, or the specific condition might be excluded.

- Scope of Coverage: A comprehensive plan that includes in-patient, out-patient, and other extras will cost more than a basic plan.

- Deductible & Co-payment: A higher deductible means you pay more before your insurance starts covering costs. Similarly, a higher co-payment means you pay more of the bill yourself. In both cases, this usually results in a lower annual premium.

- Provider Network: Plans with a “Full Network” that include top hospitals like AUBMC and Hotel Dieu usually cost more than “Limited Network” plans.

- Guaranteed Renewability: Policies that guarantee lifetime renewal regardless of your health status might have a slightly higher premium, but they offer crucial long-term security.

How to Choose the Right Health Insurance Plan in Lebanon

- Assess Your Healthcare Needs: Are you single or do you need coverage for a family? Do you have chronic conditions or plan for maternity?

- Define Your Budget: Figure out how much you can comfortably pay in Fresh USD premiums. Also, think about your ability to handle deductibles and co-payments.

- Understand Network Access: Make sure your preferred hospitals and doctors are within the plan’s network.

- Compare Coverage & Exclusions: Go beyond just the premium. Instead, compare the benefits, sub-limits, waiting periods, and specific exclusions across different plans.

- Evaluate the Insurer: Research the insurance company’s reputation for customer service and claims settlement. This is vital for a smooth and transparent process.

Conclusion: Your Partner in Health

Choosing the right health insurance in Lebanon is an important decision. It’s important because it affects your access to quality care and your financial stability. By understanding the types of coverage and evaluating your options, you can find a plan that gives you true peace of mind.

Frequently Asked Questions (FAQ)

How much does private health insurance cost in Lebanon in 2025?

Prices vary by age and coverage tier. Basic inpatient-only plans can start from approximately $350-$500 per year for young adults, while comprehensive ‘Class A’ policies can range from $1,200 to over $2,500 annually. All premiums are now strictly in Fresh USD.

Is maternity covered immediately in Lebanese health insurance?

No. Almost all private insurance policies in Lebanon impose a waiting period for maternity coverage, typically ranging from 10 to 12 months from the start date of the policy.

Does private insurance cover pre-existing conditions?

It depends on the plan. Standard policies often exclude pre-existing conditions for the first 1 to 3 years (waiting period), or permanently exclude specific chronic illnesses unless declared and accepted with an additional premium.

Why do I need private insurance if I have NSSF (Daman)?

The NSSF (Daman) coverage has been severely impacted by currency devaluation, often covering only a small fraction of actual hospital bills. Private insurance acts as a “Top-Up” (Guarantor) to cover the significant difference, ensuring you are not denied entry to private hospitals.