Table of Contents

Navigating the Lebanese Health Insurance Minefield in 2026

If you are reading this, you likely feel the same anxiety as thousands of other Lebanese citizens: the fear that despite paying premiums for years, your insurance card might be rejected at the admissions desk of a major hospital. The transition from “Lollars” to Fresh USD is now complete, but the rules of the game have changed drastically. While our general guide to health insurance covers the basics, this article is a deep dive into the technical regulations of 2026. We will explain how to secure Class A Plus care, enforce your rights under Decision 186 ICC, and avoid the hidden loyalty taxes that are draining your fresh dollar savings. For a broader overview of private health coverage options, you can also read Health Insurance Lebanon 2026 Guide.

The Fresh USD Reality

The Cash Flow Shock Explained

Gone are the days of paying in checks or LBP at the 1,500 rate. In 2026, hospitals demand immediate settlements in cash USD to pay for fuel and imported medical supplies. This has forced insurers to shift entirely to Fresh Dollar premiums. If you are still holding onto an old policy, you are effectively uninsured. Most hospitals will now ask for a cash deposit ranging from $2,000 to $10,000 before admission if your policy isn’t clearly marked as Fresh or Real USD. To understand how insurers define the settlement currency in contracts, review the legal framework in Insurance Laws in Lebanon.

Calculating the Loyalty Tax

Are you overpaying? Many insurers rely on your fear of switching to hike premiums aggressively. If your renewal premium increased by more than 15 to 20 percent this year without a claim, you might be paying a loyalty tax. Switching insurers is risky due to pre-existing conditions, but understanding your legal rights can help you negotiate. If you want a high-level market comparison, see Best Medical Insurance Companies in Lebanon.

Guaranteed Renewability GR

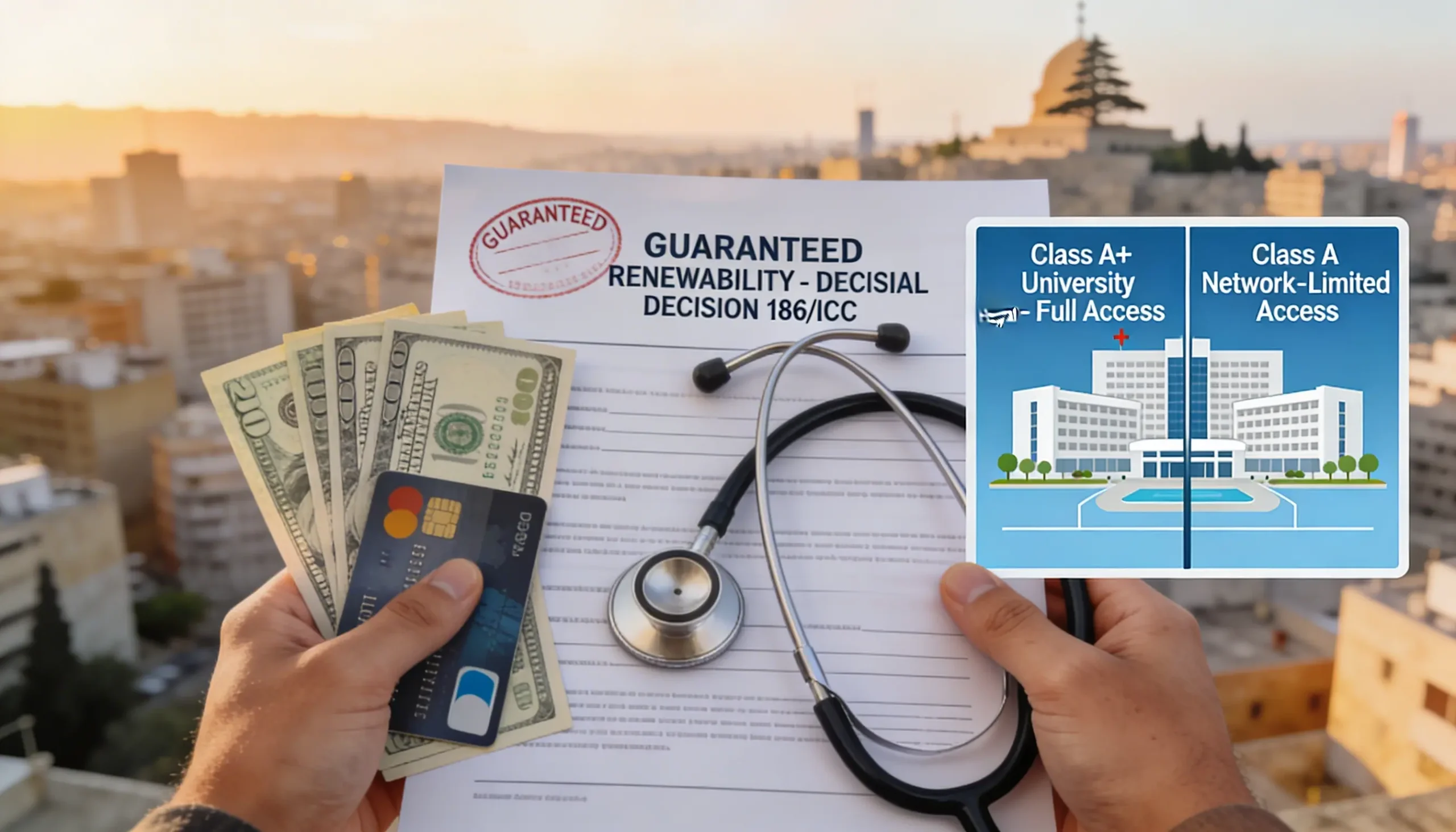

Understanding Decision 186 ICC

One of the few protections Lebanese policyholders have is Ministerial Decision No. 186 ICC. This regulation mandates Guaranteed Renewability. This means that as long as you pay your premiums on time and act in good faith, your insurance company cannot cancel your policy or refuse to renew it, even if you develop a chronic illness like cancer or heart disease. For more details on your consumer rights, read our breakdown of Insurance Laws in Lebanon.

The Continuity Clause

Terrified of switching providers because of a pre-existing condition? You should look for the Continuity of Coverage clause. If you switch from Insurer A to Insurer B with no gap in dates, you can often negotiate to carry over your time served. This means you will not have to restart the 12-month waiting period for standard illnesses.

Hospital Networks in 2026

The Class A vs University Split

Class A does not mean what it used to. Due to aggressive pricing by top-tier university hospitals such as AUBMC, CMC, and St. George, many insurers have split their networks.

- Standard Class A: Covers most private hospitals but excludes or applies a surcharge to university hospitals.

- Premium or Class A Plus: The new tier required to access top university centers with stronger coverage terms.

If your policy is Class A but you frequent Hamra or Ashrafieh, you must check your Table of Benefits specifically for the university hospital surcharge line item. You can compare the networks of the top providers in our Best Medical Insurance Companies review.

Pre-Existing Conditions

Acute Onset vs Chronic Care

For elderly parents, distinguishing between Chronic and Acute Onset coverage is vital.

- Chronic Coverage: Pays for maintenance such as dialysis and regular checkups and is expensive and less common in new policies.

- Acute Onset: Pays only when a chronic condition suddenly becomes life-threatening, for example a heart attack.

This distinction is particularly important for Expat Health Insurance plans.

Public Options: NSSF and MoPH

Despite funding injections, the NSSF acts more like a discount card than insurance. It might cover a fraction of the official rate, but the difference between the NSSF rate and the real market rate is massive. Relying on a difference of NSSF complementary policy is risky. If the NSSF delays approval or its system goes offline, your private complementary insurance might refuse to pay the primary portion. For total peace of mind in 2026, a Full Private policy is often the most reliable way to secure immediate admission.

Action Plan Before You Renew

- Check the TPA: Is your network managed by a major TPA?

- Confirm Fresh Terms: Ensure the policy wording explicitly states Fresh USD or Real USD.

- Review Day 1 Newborn Coverage: Confirm automatic newborn inclusion.

- Verify Guaranteed Renewability: Do not accept a policy without it.

- Scan for University Surcharges: Confirm full coverage or deductible levels.

Frequently Asked Questions

What is the Fresh Dollar requirement for Lebanese health insurance in 2026?

The Fresh Dollar requirement means health insurance premiums are paid in cash USD or via international transfers because hospitals demand real currency to cover imported medical supplies and fuel.

Can my insurance company refuse to renew my policy if I get sick?

No. Under Ministerial Decision No. 186 ICC, insurers are required to offer Guaranteed Renewability provided you renew within required timeframes.

Do all Class A insurance plans cover university hospitals like AUBMC?

Not necessarily. Many insurers now use a Premium or Class A Plus tier for university hospitals.

What is the difference between Acute Onset and Chronic coverage?

Chronic coverage pays for ongoing maintenance of long-term illnesses, while Acute Onset coverage pays only for sudden emergencies.